Solar Hing Printing Holdings Restricted (HKG:1975) has introduced that on twentieth of December, will probably be paying a dividend ofHK$0.043, which a discount from final 12 months’s comparable dividend. Nonetheless, the dividend yield of 8.3% nonetheless stays in a typical vary for the trade.

Take a look at our newest evaluation for Solar Hing Printing Holdings

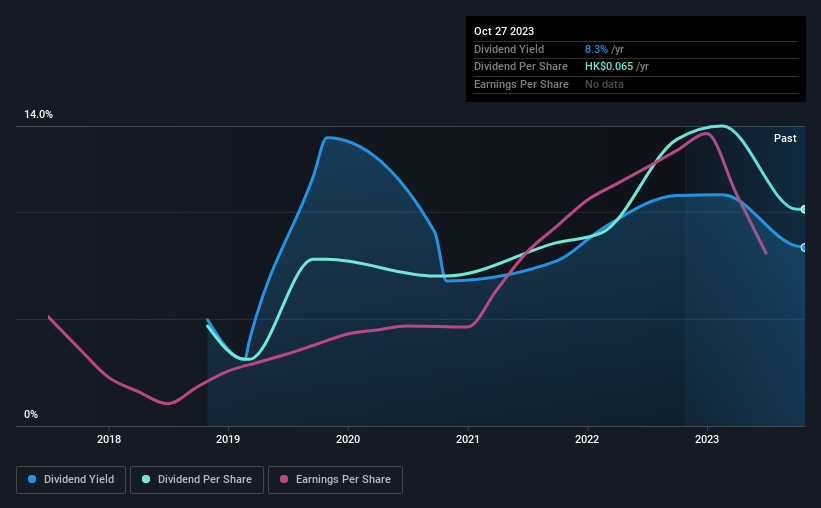

Solar Hing Printing Holdings’ Fee Has Strong Earnings Protection

Strong dividend yields are nice, however they solely actually assist us if the fee is sustainable. Previous to this announcement, Solar Hing Printing Holdings’ dividend was comfortably coated by each money stream and earnings. This means that fairly a big proportion of earnings is being invested again into the enterprise.

Over the subsequent 12 months, EPS might increase by 50.7% if latest tendencies proceed. Assuming the dividend continues alongside latest tendencies, we expect the payout ratio may very well be 32% by subsequent 12 months, which is in a fairly sustainable vary.

Solar Hing Printing Holdings’ Dividend Has Lacked Consistency

It is comforting to see that Solar Hing Printing Holdings has been paying a dividend for plenty of years now, nevertheless it has been lower a minimum of as soon as in that point. If the corporate cuts as soon as, it positively is not argument towards the opportunity of it slicing sooner or later. The dividend has gone from an annual complete of HK$0.03 in 2018 to the latest complete annual fee of HK$0.065. Because of this it has been rising its distributions at 17% every year over that point. Dividends have grown quickly over this time, however with cuts up to now we’re not sure that this inventory will likely be a dependable supply of revenue sooner or later.

The Dividend Seems to be Possible To Develop

With a comparatively unstable dividend, it is much more necessary to guage if earnings per share is rising, which might level to a rising dividend sooner or later. Solar Hing Printing Holdings has impressed us by rising EPS at 51% per 12 months over the previous 5 years. The corporate’s earnings per share has grown quickly in recent times, and it has a superb stability between reinvesting and paying dividends to shareholders, so we expect that Solar Hing Printing Holdings might show to be a powerful dividend payer.

We Actually Like Solar Hing Printing Holdings’ Dividend

It’s usually not nice to see the dividend being lower, however we do not assume this could occur a lot if in any respect sooner or later provided that Solar Hing Printing Holdings has the makings of a stable revenue inventory shifting ahead. By lowering the dividend, stress will likely be taken off the stability sheet, which might assist the dividend to be constant sooner or later. All of those elements thought of, we expect this has stable potential as a dividend inventory.

It is necessary to notice that firms having a constant dividend coverage will generate better investor confidence than these having an erratic one. On the similar time, there are different elements our readers ought to take heed to earlier than pouring capital right into a inventory. Taking the talk a bit additional, we have recognized 2 warning indicators for Solar Hing Printing Holdings that traders have to be aware of shifting ahead. Is Solar Hing Printing Holdings not fairly the chance you had been searching for? Why not try our collection of high dividend shares.

Valuation is complicated, however we’re serving to make it easy.

Discover out whether or not Solar Hing Printing Holdings is probably over or undervalued by trying out our complete evaluation, which incorporates honest worth estimates, dangers and warnings, dividends, insider transactions and monetary well being.

View the Free Evaluation

Have suggestions on this text? Involved in regards to the content material? Get in contact with us straight. Alternatively, e mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is common in nature. We offer commentary primarily based on historic information and analyst forecasts solely utilizing an unbiased methodology and our articles are usually not supposed to be monetary recommendation. It doesn’t represent a advice to purchase or promote any inventory, and doesn’t take account of your goals, or your monetary state of affairs. We intention to deliver you long-term targeted evaluation pushed by elementary information. Observe that our evaluation could not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.